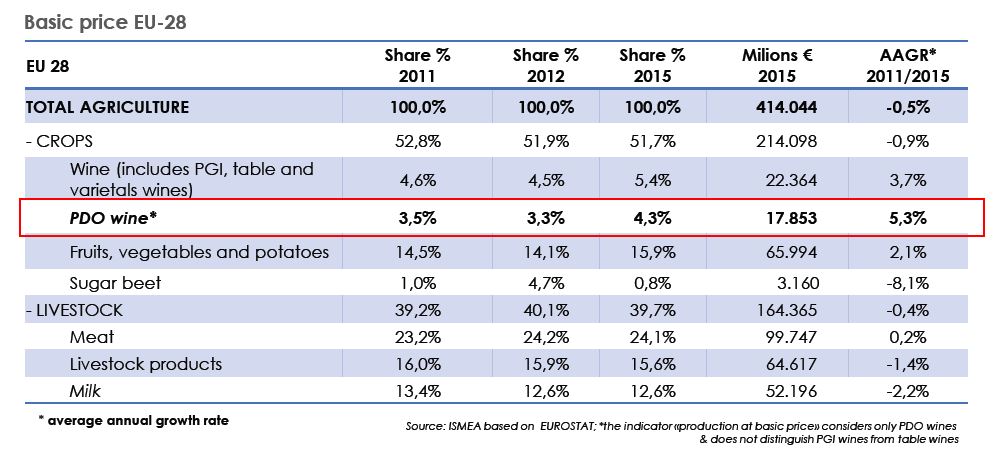

Nei mercati del Food and Beverage il vino rappresenta uno dei prodotti più globalizzati con dinamiche evolutive e di crescita che non trovano riscontro negli altri comparti, ma i vini a Indicazione Geografica comunitari evidenziano performance comunque superiori. Cresce la quota delle superficie vitate (dall’81,9% del 2012 all’83,2% del 2016), crescono i prezzi (+1% è la crescita media annua dei vini DOP e +4% quella vini IGP), l’incidenza (quella dei vini IG passa dal 62% del 2012 al 63,4% del 2016) e se il valore della produzione ai prezzi di base del vino cresce con una media annua del +4%, il tasso dei vini a IG è del +5,3%; anche l’export delle IG fa registrare incrementi del +4,2% medio annuo.

È quanto emerge dall’analisi del ruolo e delle principali dinamiche in atto per i vini DOP e IGP a livello europeo commissionata all’Ismea e presentata a Bruxelles, nel corso del “Primo congresso europeo dei vini a indicazione geografica”, organizzato dall’EFOW (European Federation of Origin Wines).

Nella Ue si contano, attualmente, ben 1.582 vini IG, di cui 1.144 DOP e 438 IGP. Le denominazioni italiane sono 526, quelle francesi sono 432. Seguono nella classifica Grecia (147) e Spagna (131). Stringendo il focus sulle tendenze in atto in Italia e Francia, i due Paesi che guidano il comparto dei vini, il valore delle produzioni atte a divenire IG tra il 2015 e il 2016 cresce in Italia (da 10,7 a 10,8 mld) mentre in Francia scende da 25,2 a 24,7 mld. Nello stesso periodo, per quanto riguarda la ripartizione del valore del vino atto a divenire IG nella Ue, cresce la quota nazionale italiana che passa dal 21,9% al 22,5%, mentre diminuisce quella francese, passando dal 51,6% al 51,2%.

Fonte: Ismea.it